-

The US president's ongoing War on Iran has raised the volume of chatter in the Energies sector over crude oil jumping to a new all-time high of $150 per barrel.

-

We've heard this before, back in 2008 to be exact, though real fundamentals are different this time around.

-

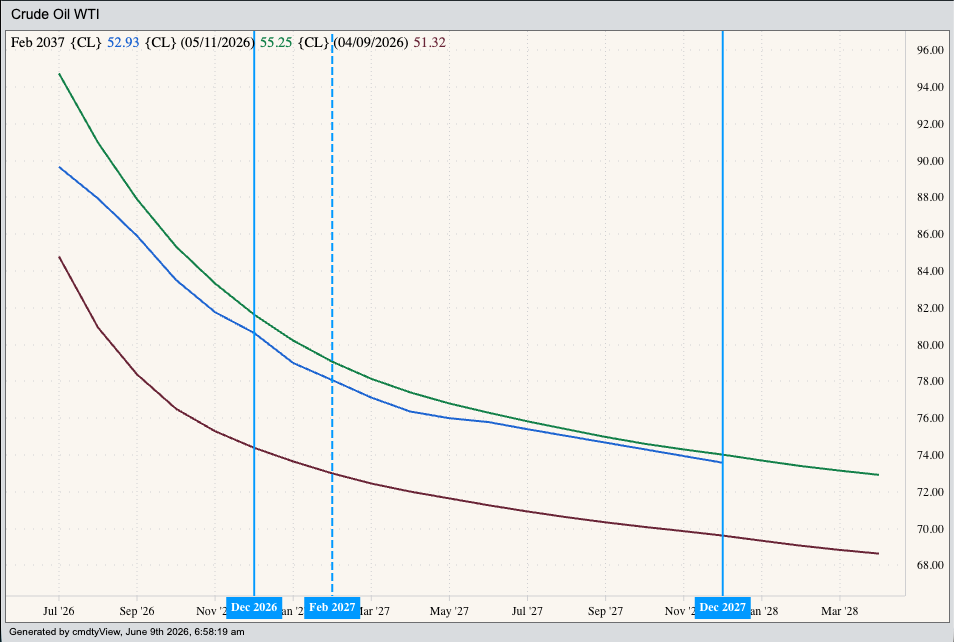

18 years ago the WTI crude oil forward curve showed a strong contango, telling us there were ample supplies to meet demand. In 2026, the forward curve continues to show strong backwardation.

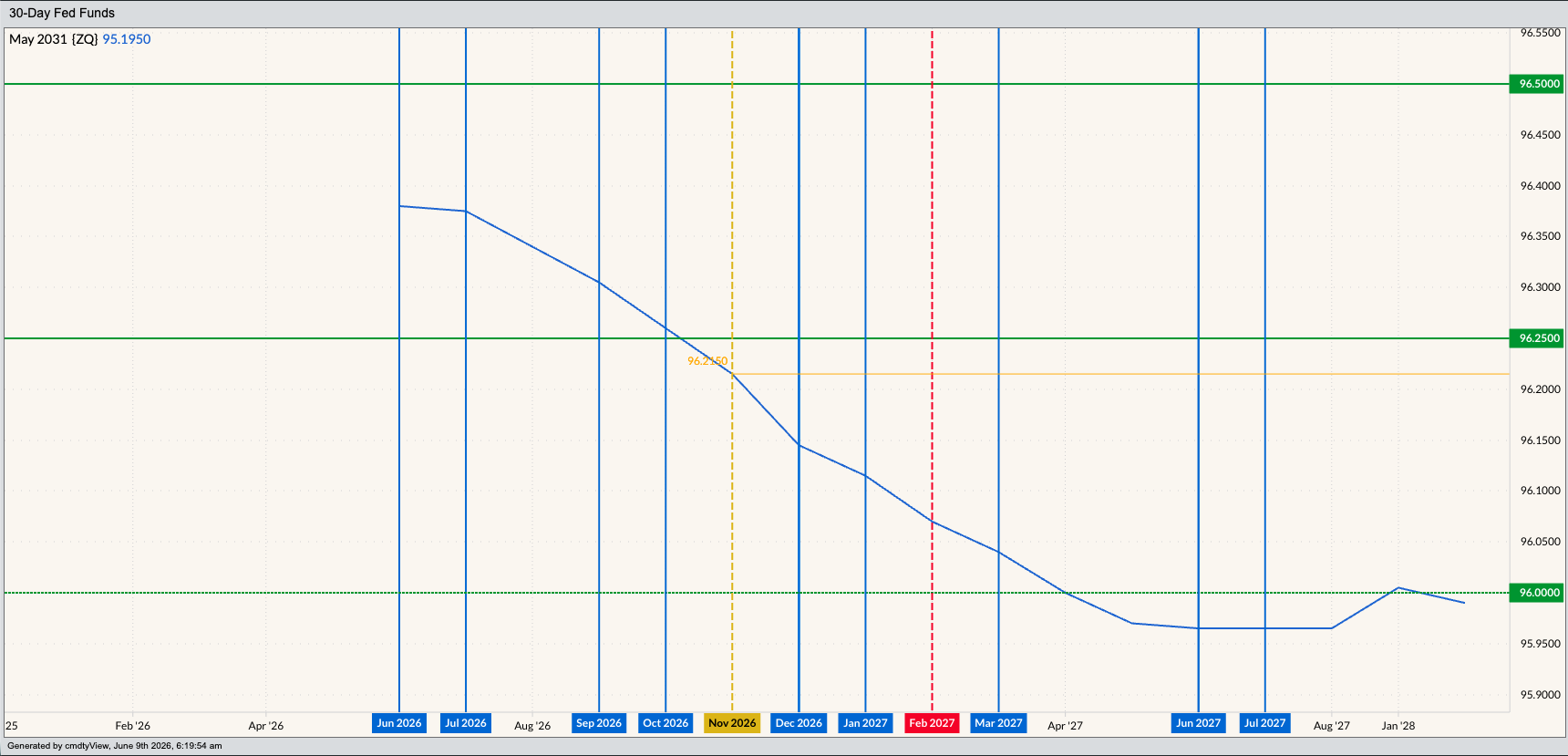

As I was putting together Morning Commentary early Tuesday, I found the typical lead headline on CNBC.com, “(The US president) says Iran deal COULD (emphasis mine) be reached in ‘two or three days’”. Yes, it is the usual nonsense we have come to expect with trade algorithms focusing on the vague “two or three days” rather than the more telling word “could”, the latter also interpreted as “could not”. We know from experience over the past decade the statement was made simply to move markets, particularly with the next US Federal Open Market Committee meeting scheduled for next week and the Fed fund futures forward curve showing the FOMC’s next move is likely to be a rate hike of 25-basis points at either the October or December 2026 meeting This move would be a response to the continued, and increased inflation problem caused by the US president’s War on Iran and one-word trade policy (tariffs) that is nothing more than a tax on US consumers.

For this discussion, I’m going to focus on the problem of inflation. A secondary headline Tuesday morning read, “Oil prices MAY (again, emphasis mine) hit $150 per barrel soon if Iran war continues, energy economist says”. Let’s take this one apart word for word:

- Logically, MAY could also mean “may not”

- Soon – a rather vague timeframe

- “If” Iran war continues. Other than Kipling’s classic poem, “If” is meaningless given the US president’s War on Iran WILL continue for the foreseeable future.

Does this mean WTI crude oil WILL hit $150 per barrel? The best possible answer I can give at this time is “Maybe”, keeping in mind there are no guarantees when it comes to market projections.

However, as most things do, this situation reminds me of a story. Back in the spring/summer of 2008[i], the WTI crude oil market was screaming higher. I was invited to do an interview on one of the CNBC programs, debating the issue with an energy trader in New York, if memory serves me (a question mark these days). The other gentleman had been projecting crude oil to hit $150 on its way to $200, again if I recall correctly, because of the market’s extremely bullish fundamentals. Believe it or not, I disagreed. The nearby futures spread was showing a strong contango (I don’t recall how strong, but it was significant), indicating the investment-led rally was unsustainable due to real fundamentals that were actually bearish. By early July 2008 the spot-month contract had climbed to $147, but then faltered, closing the month at $124. From there it was a downhill slide to the January 2009 low near $33.

My Market Rule #6 (Fundamentals win in the end) had held true once again.

Eighteen years later we are hearing the same thing. Are my thoughts on the market different this time around? From a real fundamental point of view the answer would be “Yes”. Why? The strong contango from nearly 2 decades ago has been replaced by a backwardated WTI forward curve as far out as we’d like to look. This tells us that beyond headlines being manipulated to move markets day-to-day, the commercial side of the market is concerned about supplies in relation to demand. Could this be enough to take the spot-month WTI contract (CLN26) to $150 and beyond? Again, maybe.

We have to keep in mind how incredibly stupid the Artificial Intelligence (AI) driving markets really is. The US administration knows it only has to say and/or post to not necessarily the Truth Social media key words (deal, ceasefire, delayed tariffs, etc.) to get markets to move in preferred directions. We also know the US president wants lower interest rates for personal reasons, and skyrocketing energy prices won’t make that goal easy. Therefore, things will continue to be said and/or posted to control the price of crude oil, as much as possible, regardless of the real supply and demand situation.

Left to its own devices, supply and demand would likely take the spot-month WTI crude oil contract, as well as the spot-month Brent crude (QAQ26), to new all-time highs beyond the 2008 marks of $147.27 and $148.41 respectively.

Time will tell if this is allowed to happen.

[i] This was also the summer I spoke at an energy trading conference in New York, in the shadow of the Brooklyn Bridge. I spent one evening at a watering hole watching the MLB Home Run Derby with locals.