Kimberly-Clark Corporation (KMB), headquartered in Dallas, Texas, manufactures and markets personal care products. Valued at $32.9 billion by market cap, the company’s products include diapers, tissues, paper towels, incontinence care products, surgical gowns, and disposable face masks.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and KMB perfectly fits that description, with its market cap exceeding this mark, underscoring its size, influence, and dominance within the household & personal products industry. KMB’s biggest strength is its powerful brand portfolio, with household names like Huggies and Kleenex driving loyalty and allowing premium pricing. Continued investment in R&D and new product development keeps the company ahead of consumer trends and reinforces its market-leading position.

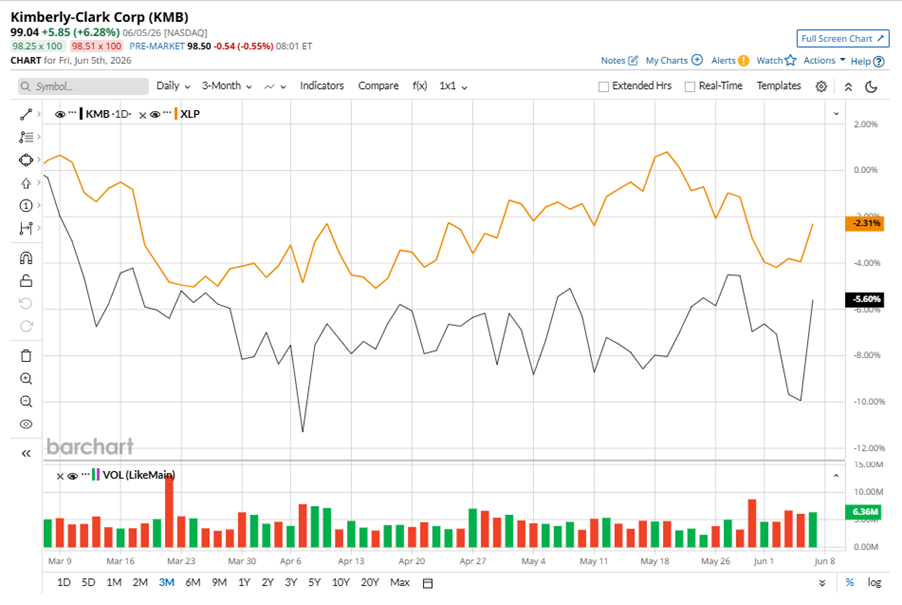

Despite its notable strength, KMB slipped 27.9% from its 52-week high of $137.46, achieved on Aug. 7, 2025. Over the past three months, KMB stock has declined 5.6%, underperforming the State Street Consumer Staples Select Sector SPDR ETF’s (XLP) 2.3% losses during the same time frame.

Shares of KMB fell 1.8% on a YTD basis and dipped 26.8% over the past 52 weeks, underperforming XLP’s YTD gains of 7.4% and 2.5% returns over the last year.

To confirm the bearish trend, KMB has been trading below its 200-day moving average over the past year, with slight fluctuations. Despite the negative price momentum, the stock has been trading above its 50-day moving average recently.

On Apr. 28, KMB shares closed up marginally after reporting its Q1 results. Its revenue was $4.2 billion, surpassing analyst estimates of $4.1 billion. The company’s adjusted EPS of $1.97 beat analyst estimates by 2.2%.

In the competitive arena of utilities - regulated electric, Church & Dwight Co., Inc. (CHD) has taken the lead over KMB, showing resilience with a 15.4% uptick on a YTD basis and 2.3% losses over the past 52 weeks.

Wall Street analysts are reasonably bullish on KMB’s prospects. The stock has a consensus “Moderate Buy” rating from the 16 analysts covering it, and the mean price target of $113.50 suggests a potential upside of 14.6% from current price levels.