If you have retirement savings in an IRA or 401(k), Uncle Sam is your partner on that money because every dollar you pull out of it is taxed.

Consider this common scenario: One spouse in a retired household passes away and the surviving spouse becomes a single taxpayer, which affects their overall tax liability, even though their income goes down.

Let's say the couple's total income was $200,000 a year. While they were married, this meant they had an effective tax bracket of about 15%.

When the husband passes away, the wife's income goes down to $180,000 because she loses the smaller of their two Social Security checks. But going forward, she will file as a single taxpayer, so she is now in the 20% tax bracket.

Additionally, if her RMDs and her income grow each year, her tax rate could keep climbing. And that doesn't even factor in future tax increases. (It's unlikely taxes will stay as low as they are now, considering our nation's debt of $39 trillion.)

Proactive tax planning could have helped protect her from the impact of higher taxes after losing her partner.

For retirees in higher tax brackets looking to help their spouse (or adult children) avoid this kind of tax trap in the future, partial Roth conversions now can help.

1. Protecting the surviving spouse

If you're a married couple, you're in a joint taxpayer bracket. And once both spouses reach age 65, you become eligible for specific additional tax benefits.

For example, with a taxable income of $148,300, you fall within the 12% tax bracket for married couples filing jointly after the deductions.

The $148,300 figure includes a $32,200 standard deduction based on your filing status. You would also receive the $3,300 additional standard deduction for both being over age 65 – this consists of $1,650 for each spouse, as determined by the One Big Beautiful Bill for taxpayers over 65. On top of this, there is an additional $12,000 bonus deduction for those over age 65 (up to a certain income limit).

However, when one spouse dies, the surviving spouse (usually the wife) jumps up to the 24% tax bracket.

If your income is higher, it's an even larger jump in taxes for the surviving spouse.

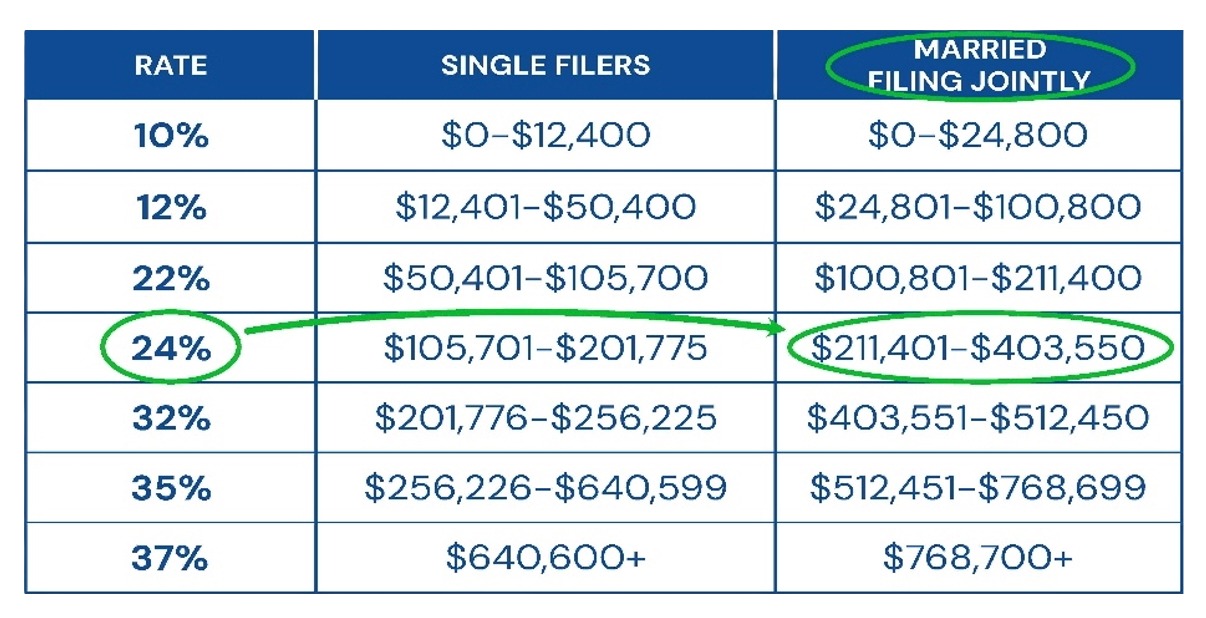

For example, if your taxable income as a married couple is $250,000 a year, you can see on the chart below that you're in the 24% tax bracket because you're "married filing jointly."

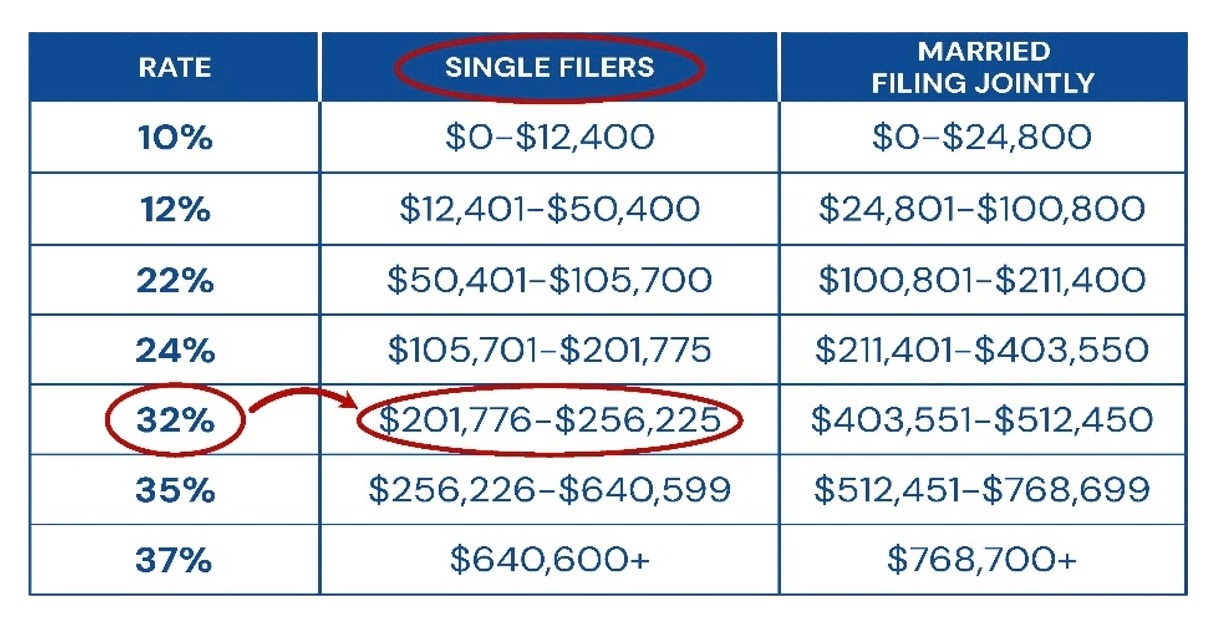

However, if the husband dies first, the surviving spouse is now a "single filer" with taxable income of $250,000. You can see she has now jumped up into the 32% tax bracket.

A Roth IRA may help protect the surviving spouse from higher taxes as a single taxpayer because you already paid the taxes while you were both alive as joint taxpayers.

2. Protecting non-spouses

When you die and leave your IRA to your children, they only have 10 years to empty your IRA completely.

Let's assume the IRA you leave to your children will earn 4% annual returns over the 10-year period after you leave it to them. This means that your children will have to take out approximately 14% of the IRA balance every year.

This would allow them to take out the 4% annual earnings along with 10% of the principal, so the entire IRA is drained over that 10-year period without a potential big tax hit in year 10.

However, this 14% annual IRA withdrawal could put your heirs in a higher tax bracket.

While a Roth conversion would mean paying income tax now, that could be a bargain compared to the potentially higher income tax brackets your heirs might have to deal with after you're gone — and any state income taxes they may also have to pay.

Additionally, if your children live in a state that has a state income tax (such as New York, which has a 10.9% top state tax bracket), they may be subject to federal income taxes and up to an additional 10.9% in state income taxes as well.

We use software called Holistiplan that helps identify the maximum amount to withdraw year by year to take advantage of today's tax brackets, and will work alongside an accountant or a tax professional.

When appropriate, we recommend our Strategic Roth Integration (SRI) plan to clients so that they can take advantage of today's income tax rates and never pay taxes on their Roth IRA again.

The appearances in Kiplinger were obtained through a PR program. The columnist received assistance from a public relations firm in preparing this piece for submission to Kiplinger.com. Kiplinger was not compensated in any way.

Related Content

- Are You Ready to ‘Rothify’ Your Retirement?

- Are Roth IRAs Really as Great as They’re Cracked Up to Be?

- Considering a Roth IRA Conversion? Six Reasons It Makes Sense

- Four Reasons to Consider Doing Partial Roth IRA Conversions Now

- Have a Retirement Bucket List? Don’t Hesitate to Dive In

This article was written by and presents the views of our contributing adviser, not the Kiplinger editorial staff. You can check adviser records with the SEC or with FINRA.