/Texas%20Instruments%20Inc_%20Santa%20Clara%2CCA%20campus-by%20Tada%20Images%20via%20Shutterstock.jpg)

For years, the race to a $1 trillion valuation in semiconductors has been dominated by flashy artificial intelligence (AI) names like Nvidia Corporation (NVDA) and cutting-edge chip designers. But one analyst believes the next company to join that elite club could come from a far quieter corner of the industry in the way of analog semiconductors. That company is Texas Instruments Incorporated (TXN).

Stifel recently highlighted that TXN may be on the path to becoming the world’s first $1 trillion analog chip stock, driven by a powerful mix of industrial recovery, booming AI data center demand, and a manufacturing strategy that competitors may struggle to replicate.

Unlike high-profile AI chipmakers chasing the latest GPU breakthroughs, Texas Instruments sits at the foundation of the digital economy, supplying the analog and power-management chips that keep everything from electric vehicles and factory automation systems to AI servers and robotics running. Analysts increasingly see positioning as a major long-term advantage, especially as AI infrastructure expands beyond just processors into power delivery, sensing, and industrial hardware.

Moreover, Stifel highlighted data centers as a major new growth driver, now contributing about 12% of revenue and approaching a $2 billion annualized run rate, with future upside tied to 800V gallium nitride power technology. The bullish thesis centers on Texas Instruments’ expanding U.S.-based manufacturing footprint, which has grown to roughly $25 billion in internal capacity, giving the company a geopolitical and supply-chain advantage ahead of the next semiconductor upcycle.

About Texas Instruments Stock

Texas Instruments is one of the world’s largest analog and embedded semiconductor companies, designing chips used in industrial automation, automotive systems, consumer electronics, communications equipment, and data centers. Headquartered in Dallas, the company has built a reputation for its long product cycles, broad customer base, and vertically integrated manufacturing strategy. With a market cap of $273.6 billion, Texas Instruments has increasingly become a key supplier to AI infrastructure and industrial markets, particularly through its power-management and analog chip portfolio.

Shares of Texas Instruments have delivered a massive rally over the past year as investors increasingly bet on a recovery in industrial semiconductors and the company’s growing exposure to AI-driven data center infrastructure. The stock is up 61.1% over the past 52 weeks, dramatically outperforming many analog semiconductor peers during that stretch.

Momentum has accelerated in 2026. TXN has gained 74.89% year-to-date (YTD), fueled by improving industrial demand trends, optimism around data center power-management chips, and Wall Street’s growing belief that the company could emerge as the first trillion-dollar analog semiconductor company. The stock also surged 32% over the past month alone as bullish analyst upgrades and stronger-than-expected commentary from management attracted fresh investor interest.

The rally pushed Texas Instruments shares to a new all-time high of $310.29 on May 14, extending a powerful breakout that began after the company reported signs of broad-based industrial recovery across the U.S., Europe, and China.

The stock trades at a premium at 39.37 times forward earnings, compared to the sector median and its historical average.

Steady Financial Performance

Texas Instruments reported strong first-quarter 2026 financial results on April 22, as the analog chipmaker benefited from accelerating demand in industrial and AI-driven data center markets. Revenue rose 19% year-over-year (YOY) to $4.8 billion, while earnings per share (EPS) climbed 31% to $1.68 from $1.28 in the year-ago quarter, comfortably beating Wall Street expectations.

The company’s core Analog segment, which remains its largest business, generated $3.9 billion in revenue, up 22% from the prior year, while Embedded Processing revenue increased 12% YOY to $723 million. Industrial revenue surged more than 30% YOY and over 20% sequentially, reflecting broad-based strength across all major geographies and sub-sectors. Data center revenue emerged as a major growth driver, jumping roughly 90% from the prior year as AI infrastructure spending accelerated.

Profitability improved sharply during the quarter. Operating profit increased 37% YOY to $1.8 billion, while net income climbed to $1.5 billion from $1.2 billion a year earlier. The company generated strong cash flow, with trailing 12-month operating cash flow rising 27% to $7.8 billion and free cash flow surging 154% YOY to $4.4 billion.

Management delivered bullish second-quarter guidance, signaling confidence that the semiconductor recovery is gaining momentum. Texas Instruments forecast Q2 revenue between $5 billion and $5.4 billion and EPS between $1.77 and $2.05.

In addition, the consensus estimate of $7.69 for fiscal 2026 indicates an increase of 41.1% YOY, before improving by around 14.2% annually to $8.78 in fiscal 2027.

What Do Analysts Expect for Texas Instruments Stock?

The optimism around the company’s accelerating industrial recovery and expanding data center business has led Stifel to raise its price target on Texas Instruments to $340 from $290 and maintain a “Buy” rating this month.

Cantor Fitzgerald raised its price target on Texas Instruments to $300 from $280 but maintained a “Neutral” rating.

Last month, BofA Securities reiterated its “Buy” rating and $320 price target on Texas Instruments after the company delivered strong first-quarter results and upbeat second-quarter guidance.

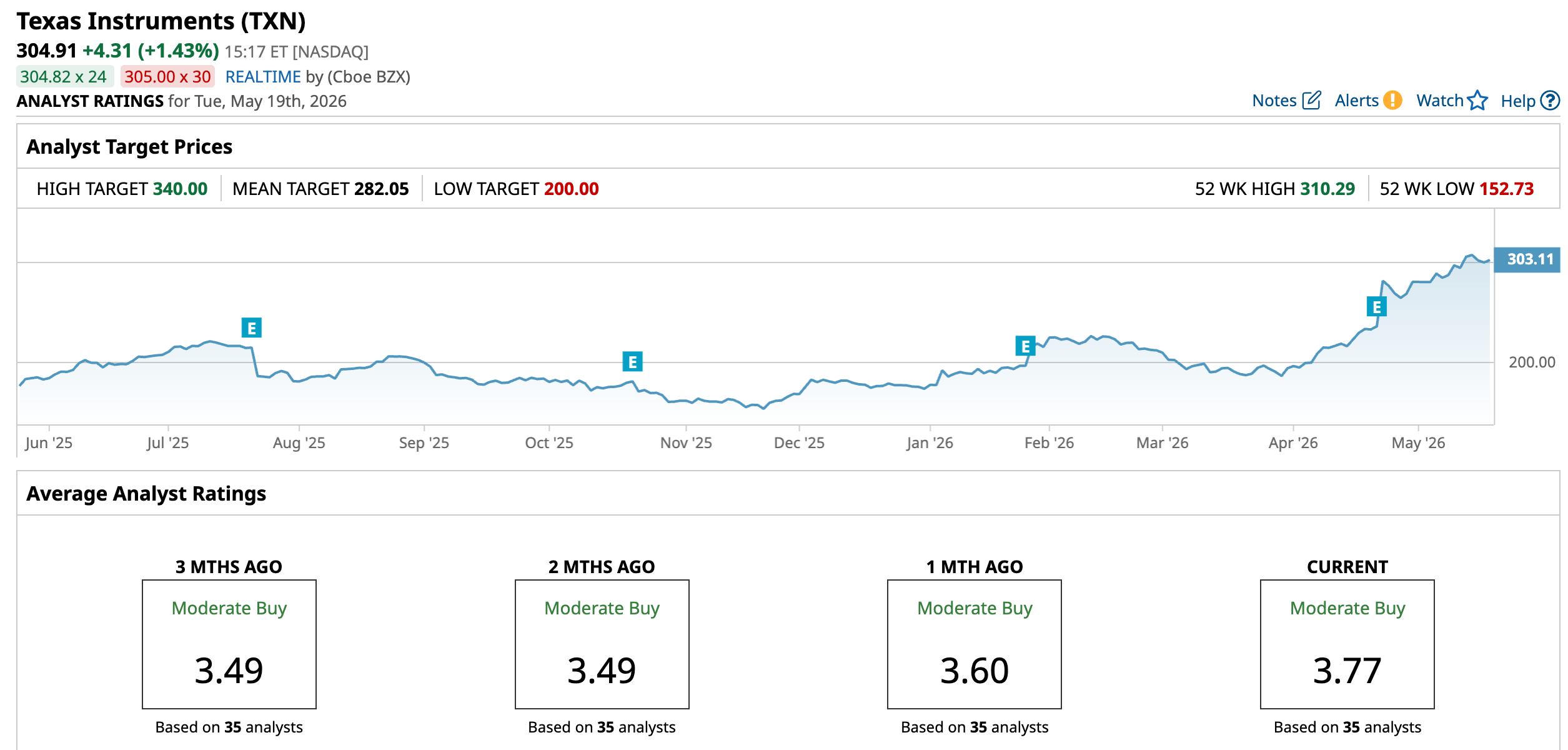

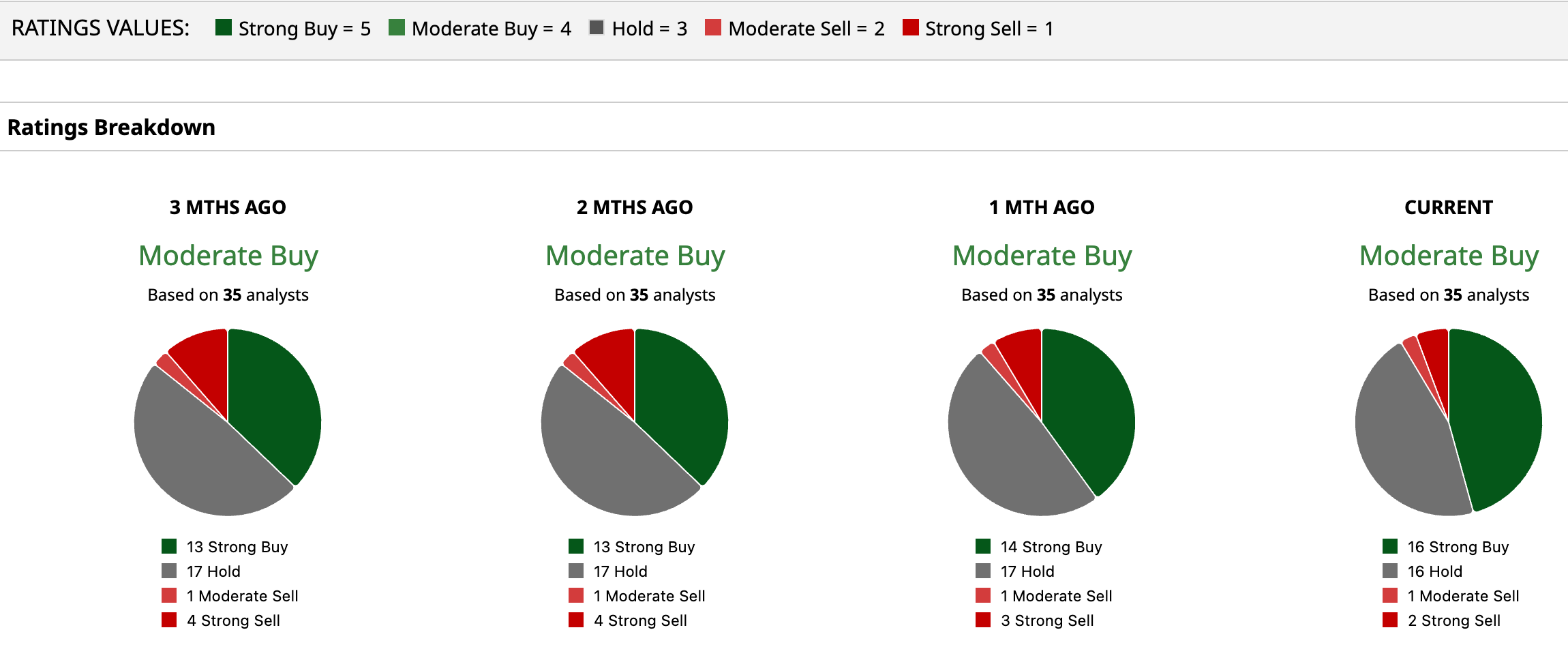

Overall, TXN stock has a consensus “Moderate Buy” rating. Out of 35 analysts covering the stock, 16 recommend a “Strong Buy,” 16 analysts stay cautious with a “Hold” rating, one advises a “Moderate Sell,” and two have a “Strong Sell” rating.

While TXN has already surged past the average analyst price target of $282.05, Stifel’s Street-high target price of $340 suggests 11.5% upside ahead.