The thrill is gone when it comes to investor interest in the Roundhill Sports Betting & iGaming ETF (BETZ). This exchange-traded fund (ETF) debuted with some fanfare back in June 2020. You’ll recall that it was near the apex of the pandemic, when workers all around the planet were looking for something to do. So they gambled. A lot. And they still are.

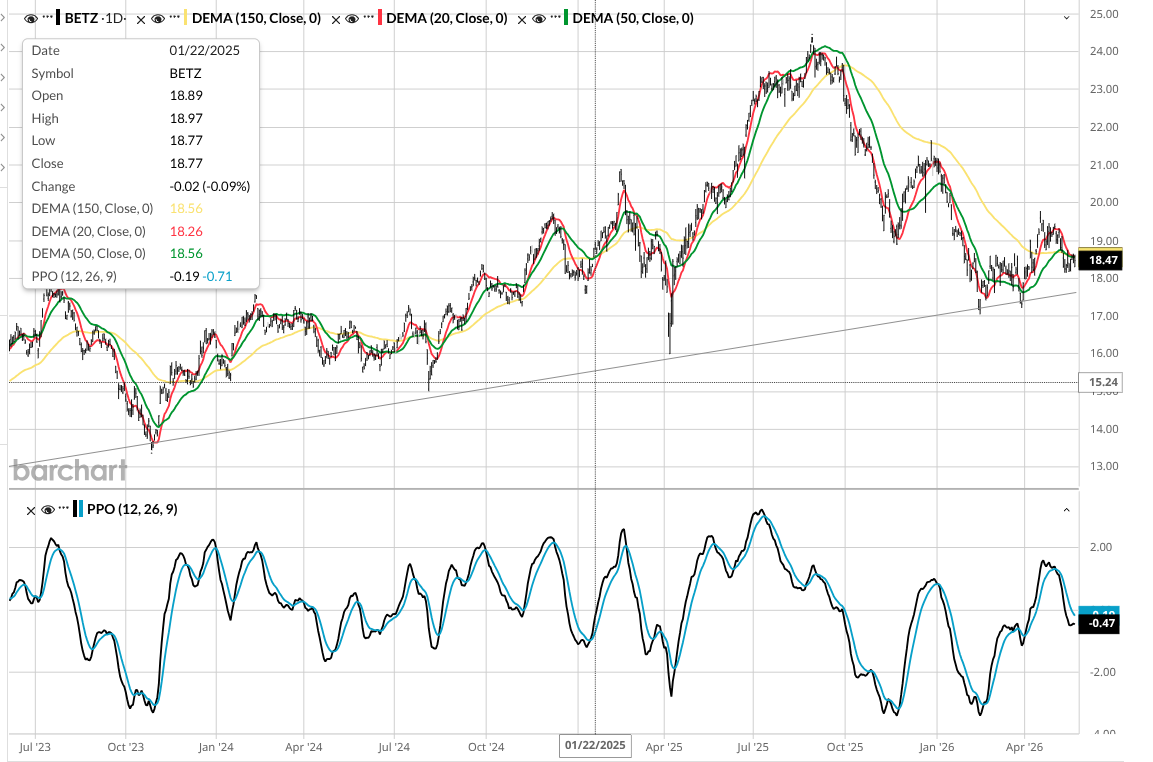

Yet BETZ has spent most of 2026 stuck in the penalty box. Assets under management (AUM) now sit at under $50 million, after peaking at nearly 10x that figure.

The fund has faced a grinding downward trend, sliding approximately 12% year-to-date. For an industry that was once treated as an unstoppable growth juggernaut, this prolonged slump has left investors wondering if the sector has permanently lost its luster or if it is quietly setting up for a major contrarian turnaround.

To understand why BETZ has struggled, we have to look at what the underlying stocks actually represent. Online gambling operators, platform providers, and digital casino giants are essentially a highly leveraged expression of consumer confidence and discretionary spending. They thrive when liquidity is plentiful, and consumers feel flush with extra cash.

With the 30-year Treasury rate stubbornly elevated and persistent inflation chewing into household budgets, the average consumer’s entertainment budget has faced a genuine squeeze. Even if high-end travel and leisure habits continue to buck that trend.

The market has responded by treating BETZ as a speculative, high-beta product that professional money managers are quick to trim during periods of macro uncertainty.

Interestingly, BETZ has been highly correlated to cryptocurrency assets over the past year. I guess that has a lot to do with them both attracting the steam time of “modern risk capital" (my term). Just as BETZ peaked in late 2021 ahead of the crypto market, its prolonged slump in early 2026 has served as an informal warning sign that broader speculative liquidity is drying up.

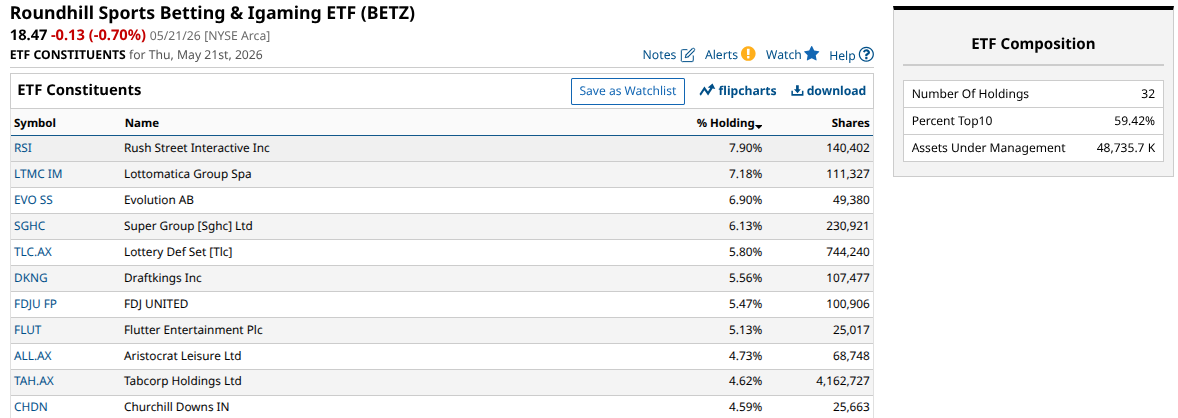

This continues to be a way to access a concentrated group of gaming stocks. Just 10 names cover nearly 60% of assets.

Why BETZ Could Stage a Second Half Comeback

Despite the messy macro backdrop, the fundamental case for a structural comeback is growing, driven by a massive, looming catalyst: the 2026 World Cup.

The World Cup is globally the single largest wagering event by total handle. Crucially, the 2026 tournament is the first in history to land in a fully legalized U.S. sportsbook market across the most populous states. This represents an unprecedented user-acquisition opportunity for the major operators inside the fund.

Because BETZ holds a diversified basket of 30 gaming stocks — including giants like DraftKings (DKNG), Flutter Entertainment (FLUT), and top holding Rush Street Interactive (RSI) — it allows investors to capture broad wagering volume without gambling on a single operator winning market share. Sportsbook earnings are notoriously lumpy based on weekly sports outcomes, but a massive structural demand event like the World Cup provides a powerful baseline for revenue growth.

The technical picture for BETZ remains fragile. The fund’s lower AUM reflects a significant drop in retail enthusiasm from its peak days. Short-term momentum indicators have turned negative, suggesting that the path of least resistance remains choppy in the immediate term.

However, from a purely strategic perspective, BETZ is becoming a compelling contrarian play. Valuations across the consumer cyclical space have undergone a heavy reset, and a great deal of bad news is already baked in here. It will likely take some time, but I am marking this one for an eventual comeback. Against all odds, if you will.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.