/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

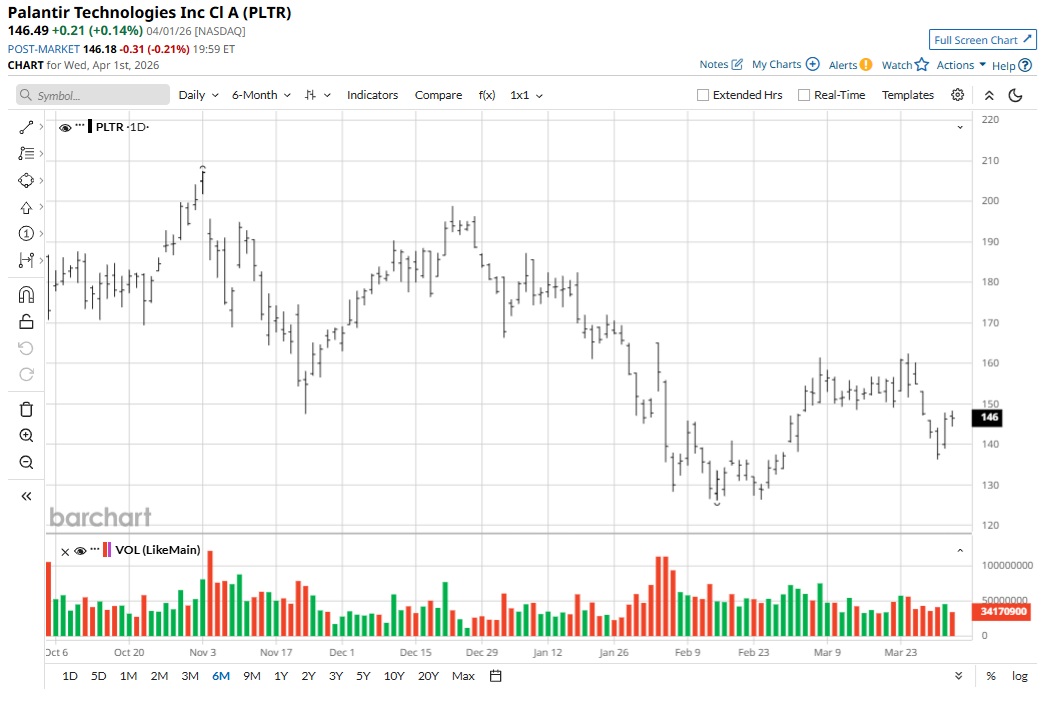

Palantir Technologies (PLTR) stock was in a steady uptrend, backed by robust growth, and touched highs of $207.52 in November 2025. However, there has been a correction of almost 30% from highs even as Palantir continues to deliver growth.

The correction has been broad-based for the technology sector on concerns related to valuation coupled with the impact of significant capex on margins. At the same time, geopolitical tensions have translated into additional risks.

Recently, Iran’s Islamic Revolutionary Guard Corps (IRGC) has threatened to attack U.S. technology companies operating in the Middle East. The IRCG considers Nvidia (NVDA), Apple (AAPL), Microsoft (MSFT), Alphabet (GOOG) (GOOGL), and Palantir Technologies among the 18 “legitimate targets.”

While this is a risk for tech stocks, U.S. President Donald Trump believes that the military campaign in Iran is likely to end in two to three weeks. Therefore, beyond the conflict, the sideways-to-lower trend in PLTR stock seems like a good buying opportunity.

About Palantir Stock

Founded in 2003 and headquartered in Aventura, Florida, Palantir initially built software for the intelligence community in the United States for assistance in counterterrorism investigations and operations. The company later diversified and started working with commercial enterprises.

Currently, Palantir has four principal software platforms: Gotham, Foundry, Apollo, and the Artificial Intelligence Platform (AIP). Through these platforms, the company served 954 customers as of December 2025.

Further, for FY25, the company reported 54% revenue from the government segment and 46% from the commercial enterprises. For the same period, 74% of the revenue was from customers in the United States.

Palantir is on a high-growth trajectory with 56% year-on-year (YoY) revenue growth in FY25 to $4.5 billion. Further, for FY25, the company’s adjusted free cash flow swelled to $2.3 billion. Amidst this growth, PLTR stock has declined by almost 21% in the last six months.

Growth Likely to Remain Robust

It’s worth noting that the Pentagon’s defense budget for FY 2026 is pegged at $1.01 trillion. Of this, a record $13.4 billion will be directed towards artificial intelligence and autonomy. Palantir is likely to be among the key beneficiaries of this allocation.

Recently, it was reported that Palantir’s Maven Smart System will be an official program of record. This is likely to ensure that Maven’s government contract size will continue to grow. Overall, the U.S. government revenue upside will be strong and support the overall growth momentum.

The commercial segment outlook also seems optimistic. As of December 2025, the U.S. commercial customer count swelled to 571, which was higher by 49% on a YoY basis. This will support top-line growth in FY26 and beyond.

Overall, Palantir ended FY25 with a total remaining deal value of the contracts at $11.2 billion. This was higher by 105% on a YoY basis. Besides providing clear revenue visibility, the growth in deal value is an indication of the business momentum across segments. Another point to note is that Palantir ended FY2025 with a cash buffer of $7.2 billion. This provides ample flexibility for investment in innovation across the company’s platforms.

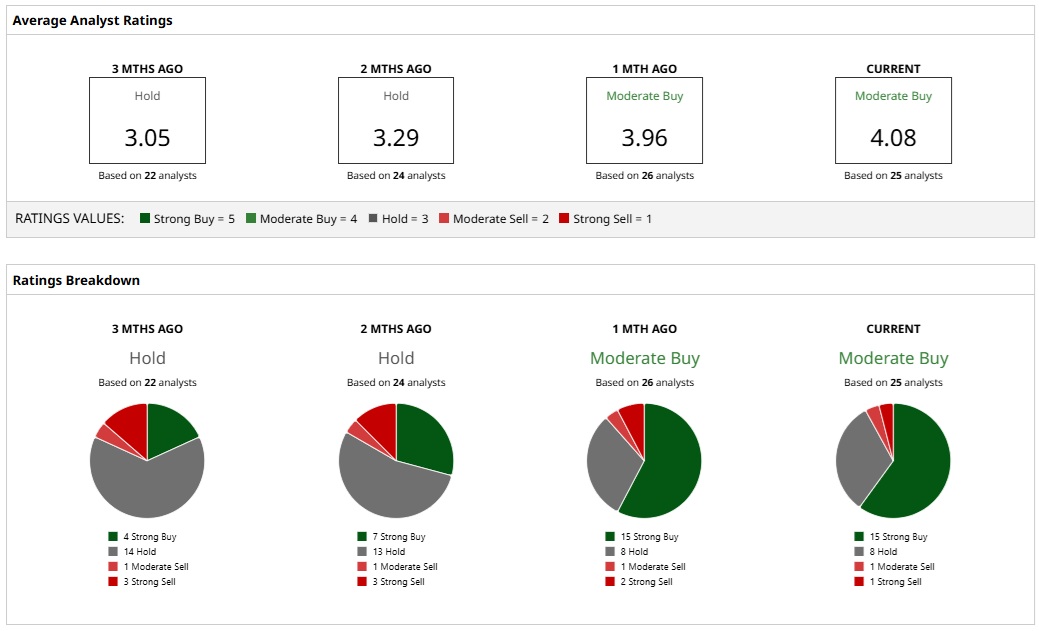

What Do Analysts Say About PLTR Stock?

Based on 25 analysts with coverage, PLTR stock has a consensus “Moderate Buy” rating. While 15 analysts have a “Strong Buy” rating for Palantir, eight analysts have a “Hold” rating. Among the bears, one analyst each opines that the stock is a “Moderate Sell” and a “Strong Sell.”

The mean price target of $201.32 represents potential upside of about 37% from current levels, while the most bullish price target of $260 suggests that PLTR could climb 78% from here.

Recently, Benchmark assigned a “Hold” rating to PLTR stock with a price target of $150. According to Benchmark analyst Yi Fu Lee, Palantir should deliver annual revenue growth in the range of 60% to 70% or “potentially face market draw down.” With swelling clients and total contract value, it’s likely that growth will be robust.