/Chubb%20Limited%20office%20sign-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

Zurich, Switzerland-based Chubb Limited (CB) provides insurance and reinsurance products and services. Valued at a market cap of $120.9 billion, the company offers an expansive suite of commercial and personal insurance solutions to a diverse client base ranging from multinational corporations to local small businesses, high-net-worth families, and individual consumers.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and CB fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the insurance - property & casualty industry. The company functions as a highly diversified risk manager capable of absorbing complex exposures on a global scale.

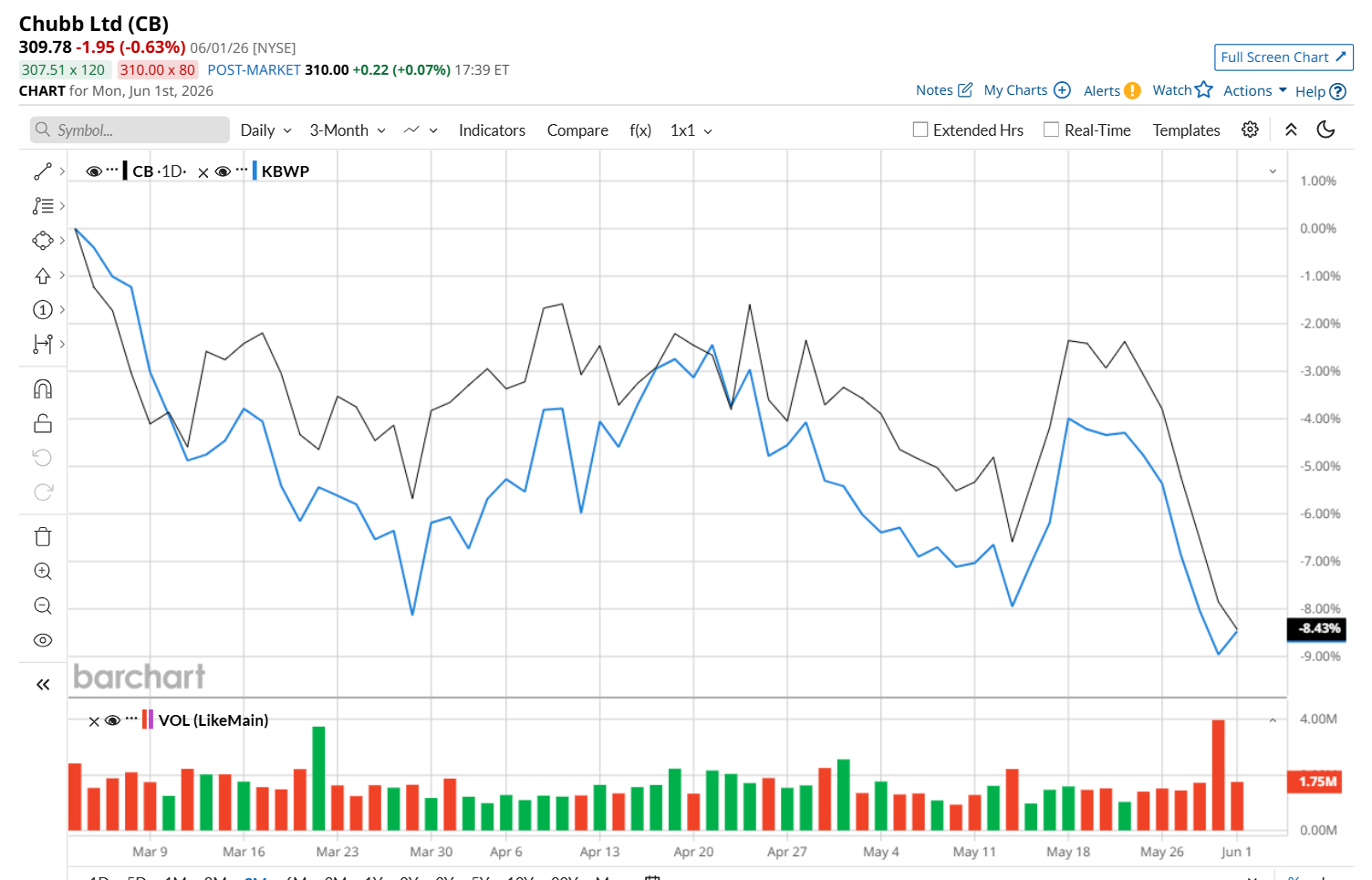

Despite its notable strength, this insurance company has dipped 10.4% from its 52-week high of $345.67, reached on Mar. 2. Moreover, shares of CB have declined 9.1% over the past three months, underperforming the Invesco KBW Property & Casualty Insurance ETF’s (KBWP) 8.3% loss during the same time frame.

However, in the longer term, CB has gained 4.2% over the past 52 weeks, outpacing KBWP's 7.6% downtick over the same time period. Additionally, on a YTD basis, shares of CB are down marginally, compared to KBWP’s 8.9% drop.

To confirm its recent bearish trend, CB has started trading below its 50-day moving average since late May. However, it has remained above its 200-day moving average since early November 2025.

Shares of CB fell 1.2% following its Q1 2026 earnings release on April 21. Driven by record investment income and low catastrophe losses, Chubb reported adjusted EPS of $6.82, which easily beat consensus estimates of $6.48. Its underlying performance also remained robust, highlighted by a 10.7% rise in consolidated net premiums written to $14.01 billion and a stellar P&C combined ratio of 84%. However, investor sentiment was slightly tempered by an increase in after-tax adjusted net realized losses, which rose to $343 million from $59 million a year earlier, alongside management's noted caution regarding softening pricing in large-account commercial property markets.

CB has outperformed its rival, The Allstate Corporation’s (ALL) 1.3% loss over the past 52 weeks. Meanwhile, it has aligned with ALL’s marginal drop on a YTD basis.

Despite CB’s recent underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 26 analysts covering it, and the mean price target of $349.42 suggests a 12.8% premium to its current price levels.