/Illinois%20Tool%20Works%2C%20Inc_%20logo%20and%20data-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Glenview, Illinois-based Illinois Tool Works Inc. (ITW) designs and produces a vast array of highly engineered components, specialized equipment, and consumable systems. It is valued at a market cap of $72.6 billion.

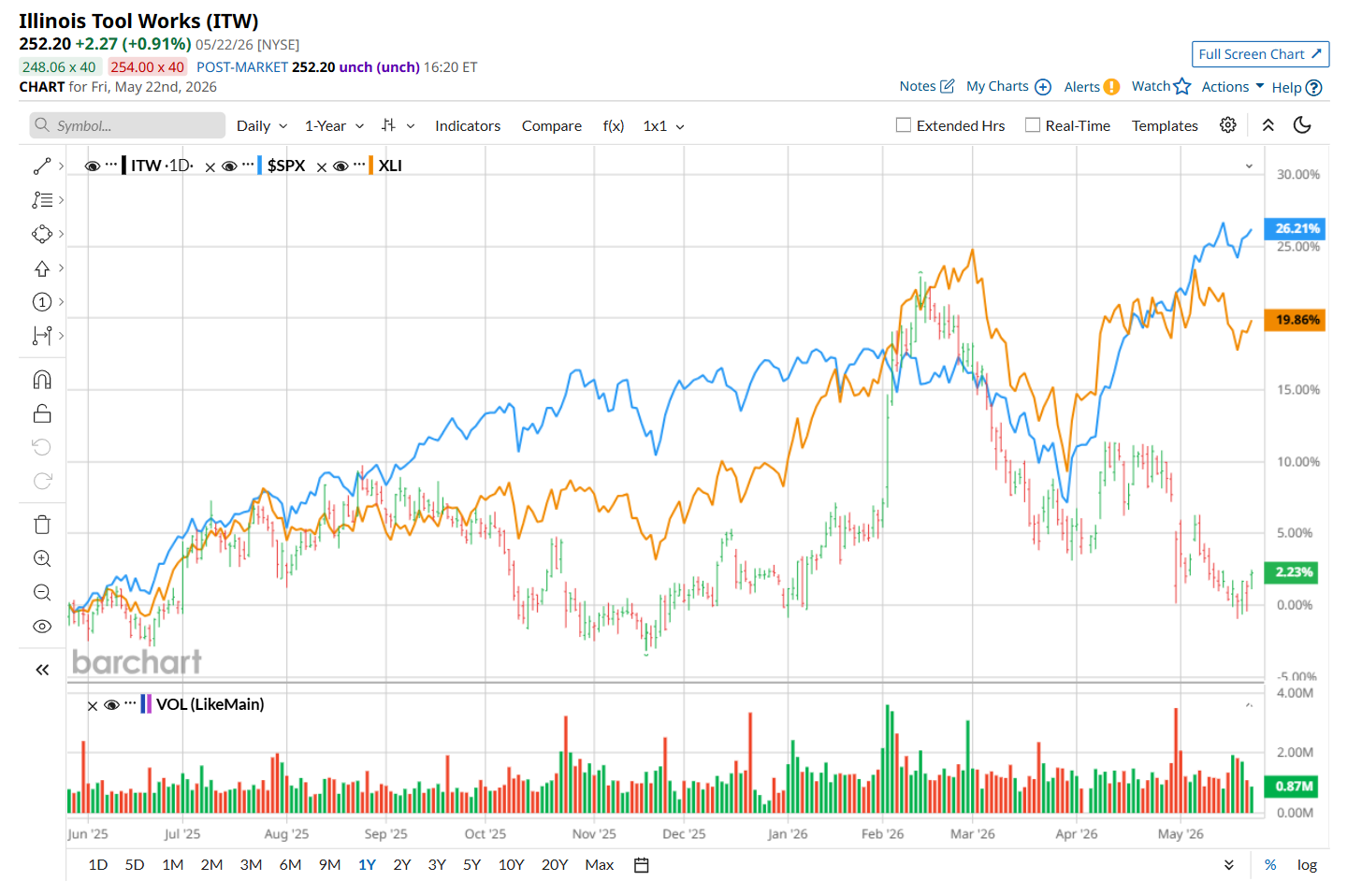

This industrial company has considerably underperformed the broader market over the past 52 weeks. Shares of ITW have gained 3.1% over this time frame, while the broader S&P 500 Index ($SPX) has soared 24.3%. Moreover, on a YTD basis, the stock is up 2.4%, compared to SPX’s 8.1% rise.

Zooming in further, ITW has also notably trailed the State Street Industrial Select Sector SPDR ETF’s (XLI) 21.6% rise over the past 52 weeks and 10.7% uptick on a YTD basis.

On Apr. 30, shares of ITW plunged 2.9% despite posting better-than-expected Q1 results. The company’s revenue increased 4.6% year-over-year to $4 billion, topping analyst estimates by a slight margin. Moreover, its EPS of $2.66 came in 4.3% ahead of consensus expectations. However, investor sentiment remained cautious due to ongoing concerns surrounding the sustainability of underlying growth. Management noted that the quarter was supported by solid demand in capital expenditure-related segments, particularly Welding and Test & Measurement, which helped offset weaker performance across consumer-focused businesses.

For the current fiscal year, ending in December, analysts expect ITW’s EPS to grow 8.4% year over year to $11.37. The company’s earnings surprise history is promising. It exceeded the consensus estimates in each of the last four quarters.

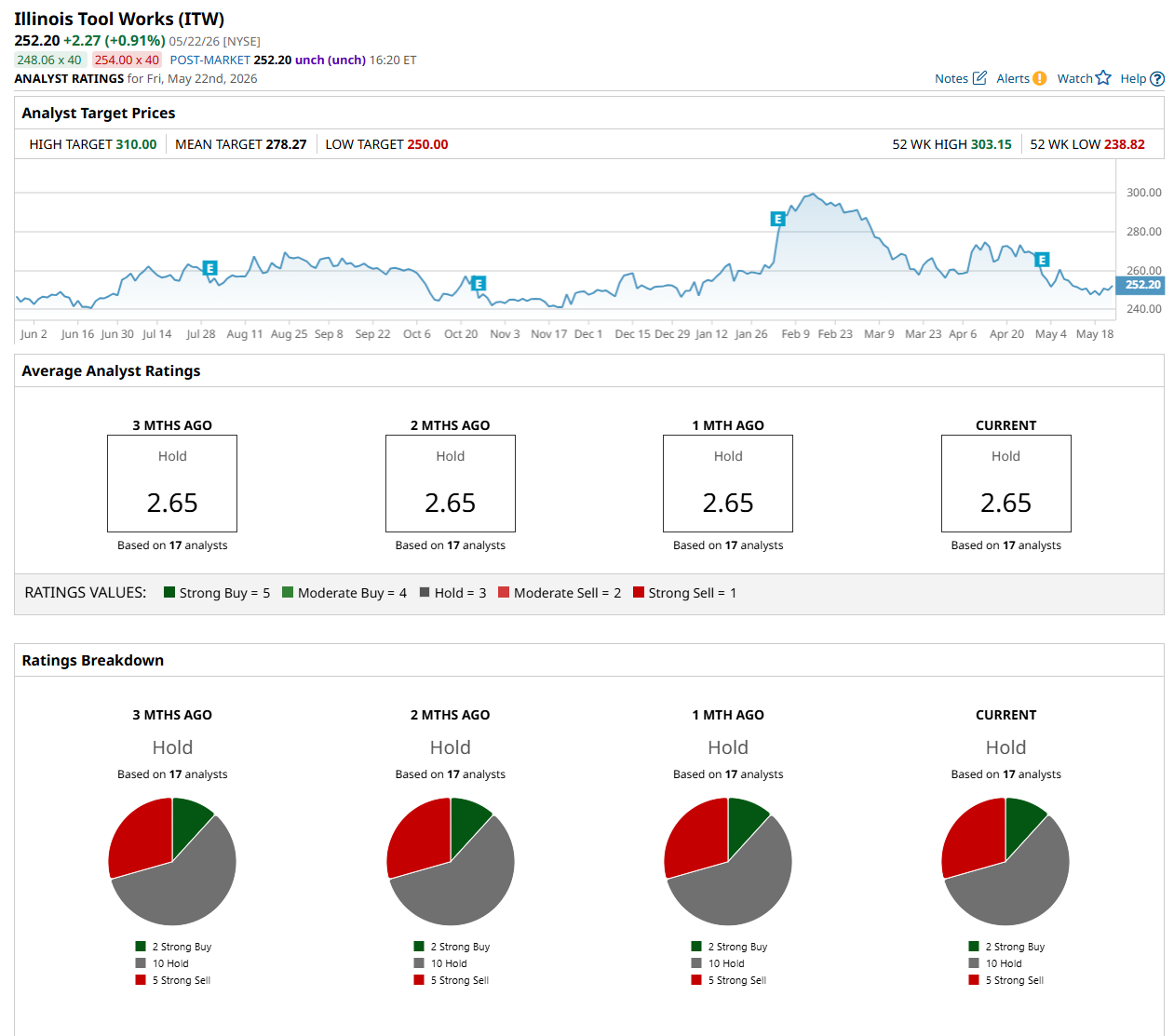

Among the 17 analysts covering the stock, the consensus rating is a "Hold," which is based on two “Strong Buy,” 10 “Hold,” and five "Strong Sell” ratings.

The configuration has remained consistent over the past three months.

On May 11, Evercore ISI maintained an "Underperform" rating on ITW and lowered its price target to $272, indicating a 7.9% potential upside from the current levels.

The mean price target of $278.27 suggests a 10.3% premium to its current price levels, while its Street-high price target of $310 implies a 22.9% potential upside.