/AI%20(artificial%20intelligence)/AI%20microchip%20by%20DesignKingBD360%20via%20Shutterstock.jpg)

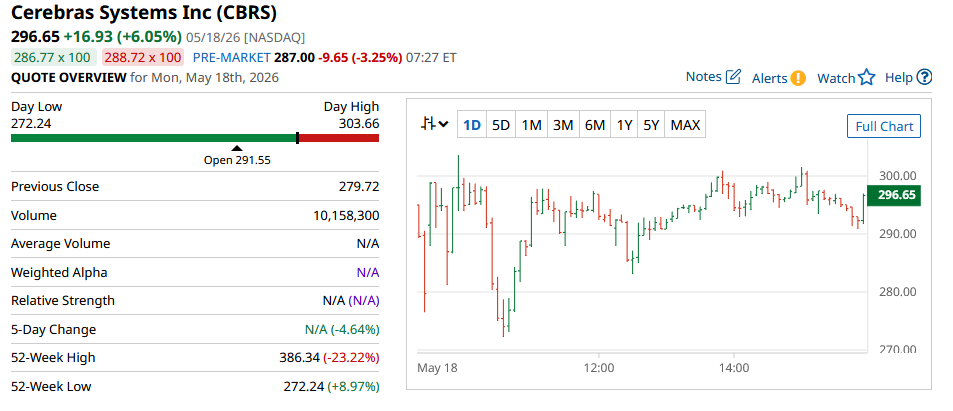

Cerebras Systems (CBRS) burst onto the scene on May 14 in a stellar IPO that saw its shares get priced at $185, well above the initial range of $115 to $125. The company raised $5.55 billion, and the stock opened for trading at $385. We’ve become used to AI stocks surging, but this one really made investors’ heads spin. As if that wasn’t enough, the stock then went down nearly 20% within the first few days of trading.

The stock gained a lot of attention primarily because of the parallels with Nvidia (NVDA), so let’s get that out of the way first. The reason people call it the next Nvidia is that the company’s product is specifically built for AI workloads. Just like Nvidia designed its GPU architecture keeping the AI training requirements in mind, Cerebras is designing its entire architecture around solving the memory bandwidth problem. Its wafer-scale engine (WSE) single-chip design reduces the interconnect losses that cause overhead in multi-GPU systems.

We know that Nvidia’s moat is significantly strengthened through its CUDA ecosystem. Cerebras is attempting something similar, though it is nowhere near the level of CUDA’s maturity yet. The potential to be the next Nvidia is there, theoretically at least. However, not all good businesses are good investments. Backing Cerebras with your money requires a deeper look, which is exactly what I am going to do today. Beyond the bells and whistles and the AI hype, I have identified two things that investors need to carefully evaluate before they back the company with their own money.

Cerebras Stock’s Valuation Is Dangerously Stretched

In the artificial intelligence era, valuations aren’t given as much respect as in the past. Investors are happy to pay any multiple as long as the stock is part of the AI trade. The same is happening with CBRS, but the valuation is too high for comfort. The company reported 2025 revenues of $510 million. The YoY growth was 76%, which is impressive. Let's assume the company continues to grow at the same rate in 2026, reaching an annual revenue of about $900 million. At the market cap of $63 billion, investors are paying 70 times the forward sales!

For context, Nvidia’s forward price-to-sales multiple is 14.4x while Advanced Micro Devices (AMD) trades at a multiple of 13.9x. This is quite a rich valuation for a stock that still has a lot to prove. Paying five times more than the multiples of Nvidia and AMD isn’t a bet that is going to bring in life-changing results, making Cerebras quite a risky play here.

Cerebras' Lock-Up Structure Creates Immediate Selling Pressure

Many investors are familiar with the 180-day lock-up period, where initial investors of the company aren’t allowed to sell their stock post-IPO. If you thought the same was the case with Cerebras, think again. The company has a unique lock-up period, and once you realize how it is set up, you may want to step away from the stock altogether.

The company’s lock-up releases are tied to earnings dates rather than a fixed 180-day period. When it announces its Q1 2026 earnings, insiders can sell up to 30 million shares. On the second quarter’s earnings call, they can sell another 30 million. The quantum is important here because 30 million is exactly the amount of common stock the company sold in the IPO. If you think about it, potentially twice the amount of shares sold in the IPO could flood the market within a few months. The increased supply is going to depress the stock price, and if the hype dies down, IPO frenzy buyers will have to wait a long time at the current valuation to get back to break-even.

About Cerebras Systems

Cerebras Systems is an AI infrastructure company that designs and manufactures an AI compute platform for deployment in data centers. The firm is known for its wafer-scale engine, which is a chip design that allows higher speed and performance compared to traditional GPUs powering the AI training infrastructure. The company is seen as benefiting from the AI inference demand, though it has yet to prove its worth in the market. It was founded in 2015 and is based in Sunnyvale, California.

The company’s stock opened for trading at $350, but has since come down below $300 in two trading sessions since the IPO. It is expected to receive fast-track inclusion in the S&P Dow Jones Indices, which could drive some optimism in the short-term. The firm is yet to announce the date for the Q1 2026 earnings report.