/Applied%20Materials%20Inc_%20logo%20on%20phone-by%20sdx15%20via%20Shutterstock.jpg)

Headquartered in Santa Clara, California, Applied Materials (AMAT) is one of the world’s premier semiconductor and display equipment manufacturers. Founded in 1967, the company specializes in atomic-level materials engineering systems that allow global chipmakers to fabricate increasingly complex integrated circuits. Applied Materials provides the highly advanced deposition, etching, and ion implantation tools required to produce some of the most advanced microprocessors on the planet.

Applied Mateirals recently reported second-quarter earnings. Here's what investors should know.

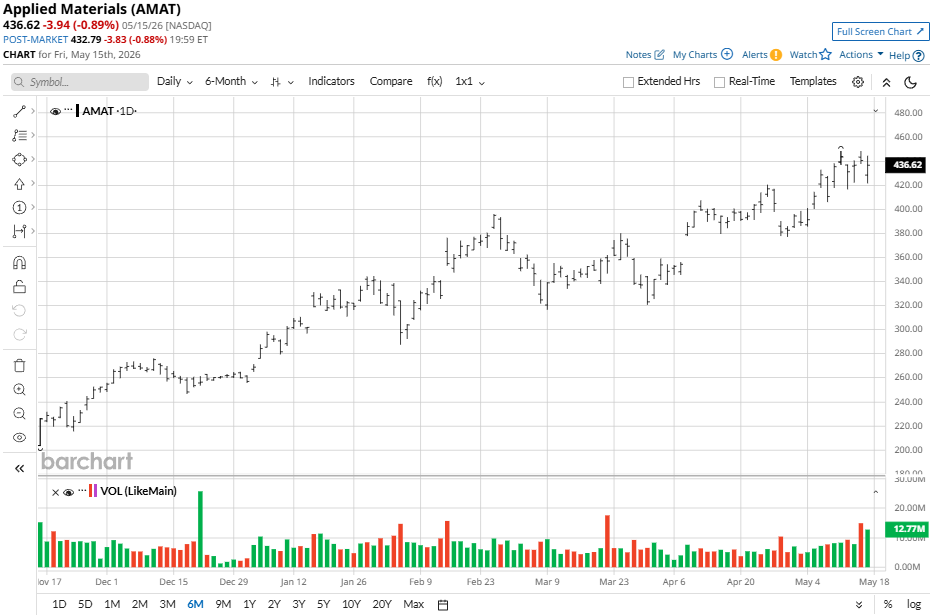

Applied Materials Hits All-Time Highs

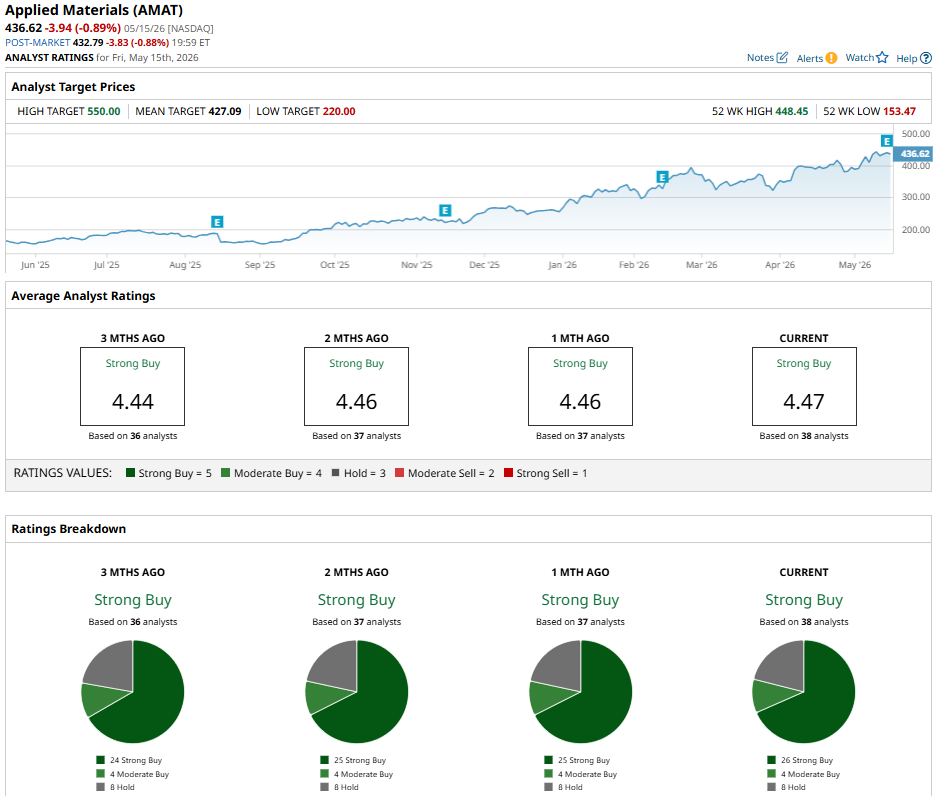

Applied Materials stock has been propelled by an aggressive capital expenditure cycle across the broader semiconductor sector. Shares have experienced an exceptional multiyear bull run, recently peaking at an all-time high of $448.45 on May 14. Investors have heavily accumulated AMAT stock from a 52-week low of $153.47, pricing in a permanent valuation rerating.

The S&P 500 Information Technology ($SRIT) benchmark has achieved strong double-digit returns driven by cloud computing and enterprise software expansions. However, AMAT stock has outperformed the broader index, up a staggering 140% over the past 52 weeks versus the benchmark's gain of 43% over the same period. Year-to-date (YTD), AMAT is up 58% while SRIT is up 15% in 2026.

With a high beta of 1.66, AMAT exhibits significantly greater price volatility than the standard index, exposing portfolio holders to sharper short-term pullbacks during sector-wide consolidations. However, Applied Materials' direct leverage to physical hardware manufacturing infrastructure has cemented it as a clear leading alpha generator.

Applied Materials Beats Q2 Estimates

Applied Materials delivered a phenomenal financial performance for its fiscal second quarter reported on May 14, obliterating Wall Street expectations across all primary metrics. Total revenue hit a record $7.91 billion, representing an 11% increase year-over-year (YOY) and comfortably outperforming the analyst consensus of $7.65 billion.

Profitability reached historic milestones with a stellar non-GAAP gross margin of 50%, its highest in over 25 years, alongside a non-GAAP operating margin of 32.1%. Non-GAAP diluted EPS also beat estimates, surging 20% YOY to $2.86, driven by relentless institutional tool demand.

The company's performance was heavily anchored by the Semiconductor Systems division, fueled by rapid global data-center updates and advanced manufacturing configurations. Operationally, the firm generated $845 million in cash from operations and distributed $765 million to shareholders, which included $400 million in opportunistic share repurchases and $365 million in dividends.

Highlighting intense forward visibility, Applied Materials authorized a 15% dividend increase to $0.53 per share. Management also announced the planned acquisition of ASMPT's (ASMVY) NEXX unit to dramatically expand its proprietary portfolio of panel-level advanced packaging technologies, which are essential to building larger-body AI accelerators.

Looking ahead, management provided an exceptionally bullish outlook. CEO Gary Dickerson forecast the core semiconductor equipment business to grow more than 30% in calendar-year 2026. The explosive global deployment of generative AI computing architectures has resulted in critical wafer tool supply deficits extending deep into 2027.

Backed by its new Precision Selective Nitride toolsets and multi-year collaborative partnerships with Taiwan Semiconductor (TSM), SK Hynix, and Micron Technologies (MU), Applied Materials has a rock-solid operational foundation to sustain high-margin market share leadership and revenue acceleration throughout the fiscal year.

Should You Bet on AMAT Stock?

Applied Materials’ record-breaking Q2 results and 50% gross margin beat underscore its dominance in the hardware infrastructure boom, proving its engineering is vital for the next generation of AI chips.

AMAT stock maintains a definitive consensus “Strong Buy” rating. Out of 38 analysts with coverage, 26 have a “Strong Buy” rating, three have a “Moderate Buy,” and nine analysts have a “Hold” rating. The mean price target of $488.85 suggests potential upside of 20% from current levels.

All told, while shares may consolidate near recent all-time highs, AMAT stock remains an exceptional long-term bet for investors seeking foundational exposure to global semiconductor manufacturing.