/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

Alibaba Group Holding (BABA) is a global conglomerate specializing in e-commerce, retail, cloud computing, and digital media. The company commands a dominant position in the Chinese digital economy through its core online marketplaces, Taobao and Tmall. Beyond its foundational e-commerce footprint, Alibaba has transformed into a critical infrastructure provider via its Cloud Intelligence Group.

Founded in 1999, the company is headquartered in Hangzhou, China.

BABA Stock Continues to Struggle

Alibaba's stock price reflects the ongoing volatility of China's economic recovery. The equity is trading around $134.47, pushing off a 52-week low of $103.71 while retracing from its 52-week high of $192.67. Over the past 12 months, the asset has registered a stable 7.4% return. However, intense competition and massive capital expenditures on AI chip development have weighed on near-term valuations, causing a 12% year-to-date decline. Over a longer horizon, geopolitical and regulatory overhangs persist, leaving the stock with a negative 37% five-year return.

Compared with the broader market, Alibaba continues to trade at a deep valuation discount. While domestic equity indices have steadily climbed on mega-cap tech expansion, Alibaba’s year-to-date contraction highlights a decoupling from broader market momentum.

Alibaba In-line with Analyst Estimates

Alibaba reported resilient fourth-quarter results on May 13, underscoring an aggressive, investment-heavy operational pivot toward next-generation tech. Total quarterly revenue rose 3% year-over-year to $35.28 billion, matching consensus estimates.

Growth was primarily turbocharged by a major structural acceleration within the Cloud Intelligence Group, which saw its external revenue surge 40% year-over-year. Crucially, AI-related product revenue delivered triple-digit growth for the 11th consecutive quarter, now contributing 30% of total external cloud sales and validating management's deep tech ambitions.

However, aggressive ecosystem scaling heavily pressured core segment profitability. Adjusted EBITA plummeted 84% year-over-year to $740 million due to large investments in quick commerce, user acquisition for the Qwen personal assistant app, and expansive overseas infrastructure. Conversely, GAAP net income jumped 96% to $3.41 billion, driven by sharp mark-to-market valuation gains on equity investments, while non-GAAP diluted earnings-per-ADS came in at $0.09. Backed by an enormous net cash position of $38 billion, management approved an annual dividend of $1.05 per ADS.

Looking ahead, management expects model and application services annualized recurring revenue to surpass $4.3 billion by year-end, positioning AI as the primary engine driving long-term corporate growth.

Alibaba Doubles Down on AI

Alibaba’s semiconductor subsidiary, T-Head, has released its latest Zhenwu M890 AI chip. A powerful training and inference chip designed to strengthen China’s domestic hardware ecosystem. The latest M890 delivers three times the performance of its predecessor, the Zhenwu 810E, while being equipped with 144 GB of GPU memory and an inter-chip bandwidth of 800 GB per second. This specific architecture makes the chip precisely optimized to handle complex agentic AI workloads demanding vast context retention and rapid processor communication.

Alibaba has already shipped over 560,000 units of its Zhenwu chips to over 400 enterprises across 20 industries, showcasing its strong commercial traction. Besides the Zhenwu chips, Alibaba also announced the release of its next-gen large-language model (LLM), the Qwen 3.7-Max.

This dual launch allows Alibaba to build an independent and fully integrated AI platform bridging proprietary silicon, cloud infrastructure, and frontier models with AI products expected to drive half of its cloud business revenue within the year.

Should You Buy BABA?

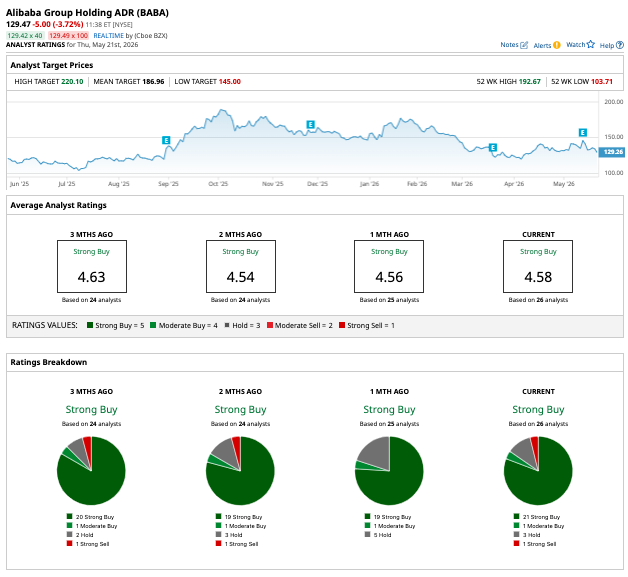

The unveiling of the Zhenwu M890 AI chip and the Qwen3.7-Max LLM underscores Alibaba's aggressive transformation into a vertically integrated AI powerhouse. While heavy infrastructure spending currently pressures short-term margins, Wall Street remains overwhelmingly bullish on this structural pivot, awarding the stock a consensus "Strong Buy" rating. Out of 26 analyst ratings, a commanding 21 recommend a "Strong Buy," alongside one "Moderate Buy," three "Holds, and just one "Strong Sell."

With a mean price target of $186.96, Alibaba offers a 44% projected upside from its current market price, making it an incredibly attractive deep value play on China's localized AI infrastructure boom.