/Micron%20Technology%20Inc_logo%20and%20website-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)

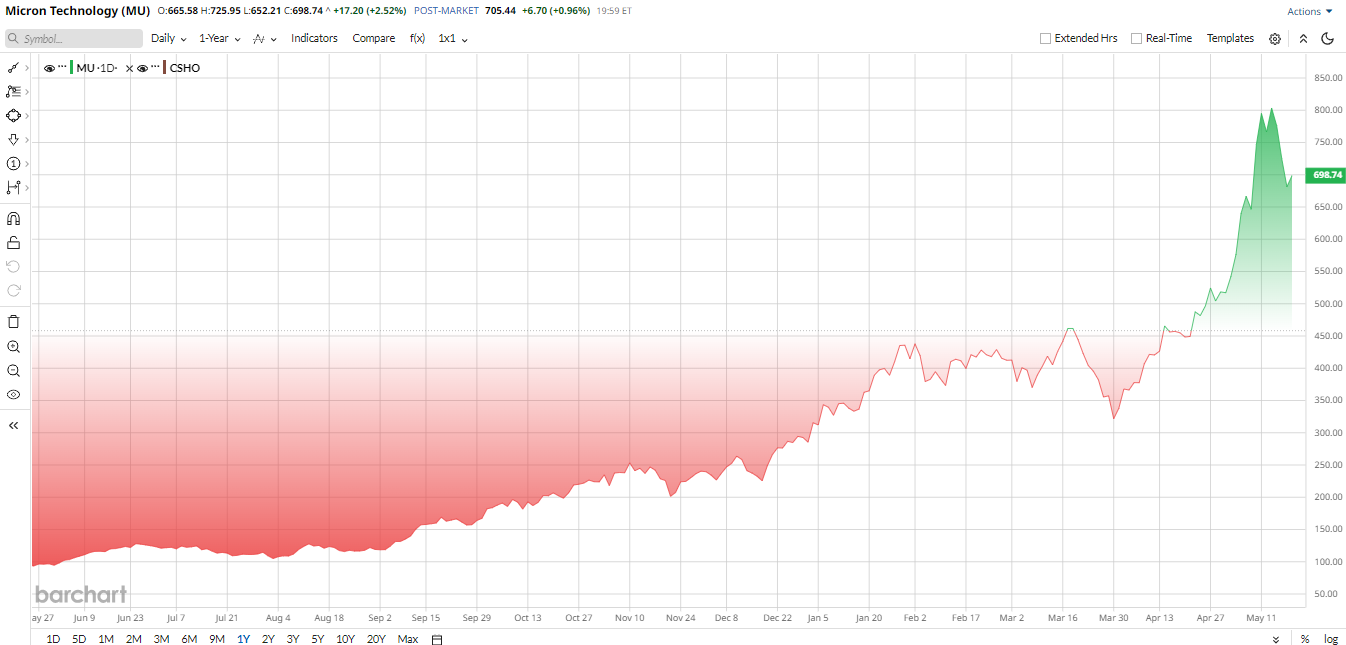

Micron Technology (MU) is back in the market’s good graces, and the rally is gaining momentum. Shares climbed on May 19 as investors leaned into a strengthening memory-chip pricing cycle, even as the Nasdaq slipped and rising bond yields pressured growth stocks.

The bullish sentiment makes sense. MU stock has surged this year alongside booming AI-driven demand, and analysts expect DRAM prices to keep climbing. Earlier this month, Citi raised its price target on Micron to $840 from $425, citing expectations for DRAM prices to nearly triple next year.

Industry data supports the outlook. Contract DRAM prices have jumped 58% to 63% over the past quarter, while Gartner forecasts DRAM pricing could rise another 125% in 2026. Adding to the bullish case, Etron Technology Chairman Nicky Lu recently said supply remains tight, with prices still increasing 10% to 20% a month.

In this environment, Micron appears well-positioned to capitalize on one of the strongest memory markets seen in years.

What's Happening With Micron Stock?

Micron stock has been on a tear lately, surging roughly 165% in 2026 and 688% over the past year. Investors have piled into MU stock as AI demand has boosted memory-chip sales, DRAM supply has tightened, and prices have kept rising. Analysts have also turned more bullish on Micron’s future earnings growth, with predictions of $18.97 in EPS for the upcoming quarter. That would mark an almost 1,000% increase year-over-year (YOY).

Despite the massive run-up, MU stock looks cheap on some metrics. The stock trades at around 12 times forward earnings, far below the industry average, and about 32 times trailing. At the same time, its price-to-sales (P/S) ratio is 21 times, which is well above the sector median. In short, Micron’s earnings yield is very high, but investors are already paying up for each dollar of revenue.

DRAM Market Outlook and Impact on Micron

Analysts are united on the idea that a memory bull market is underway. Besides Citi’s forecast, Morgan Stanley noted in February that DDR5 DRAM spot prices were about 130% above contract levels this year, with contract rates already up 86% since December. The bank believes supply shortages will keep prices rising, and with supply growth slowing, further hikes are expected.

This pricing power is a huge tailwind for Micron. Higher DRAM average selling prices (ASPs) flow straight to the company's top line. This means each chip it sells yields more profit, and Micron has signaled it will pass on those gains. In practice, this has driven recent surges in revenue and profit.

Mircon Tops Q2 Earnings Estimates

Micron’s second-quarter results showcased the boom. For Q2, revenue leapt to $23.86 billion, nearly triple the $8.05 billion from a year earlier. EPS hit $12.20 versus $1.56 a year ago. Adjusted free cash flow was a hefty $6.9 billion, while cash on hand stood at about $16.7 billion at quarter’s end.

CEO Sanjay Mehrotra said that the company “set new records across revenue, gross margin, EPS, and free cash flow” thanks to strong demand and tight supply. The company raised its dividend by 30% to show confidence in continued strength. All business units — cloud, data center, mobile, and auto — saw huge YOY jumps in sales, with most roughly doubling or more.

Management forecast another blowout Q3. Guidance calls for about $33.5 billion in revenue and roughly $19 in EPS. That outlook implies further massive growth, and it tops analysts’ own hopes. Analayst revenue estimates for Q3 span roughly $33 billion to $40 billion as experts gauge just how fast AI-driven spending will climb. For the full year, Wall Street’s outlook is now very high; fiscal 2026 revenue is expected to be about $109.7 billion and EPS to be roughly $58, up from much lower estimates just a month earlier.

In short, Micron’s latest results and guidance far exceeded the norm for semiconductor firms, showing the upside from rising DRAM prices.

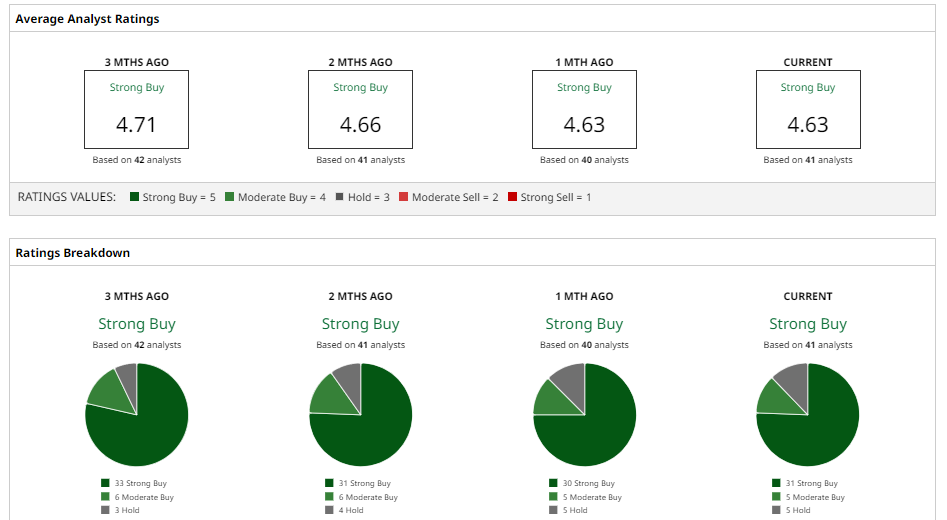

What Do Analysts Think of MU Stock?

Wall Street is overwhelmingly positive on MU stock. Citi analysts have a “Buy” rating and a price target of $840. While Morgan Stanley recently raised its target to $520 and UBS now sees $535 per share, Deutsche Bank has a $1,000 target and HSBC has a $1,100 target. Meanwhile, Mizuho has a target of $800.

Overall, analysts have a consensus "Strong Buy" rating on shares. However, MU stock is currently trading higher than its mean price target of $628.20, which suggests downside risk. Still, analysts stress Micron’s pivotal role in AI data centers. Research notes that customers are locked into long-term supply agreements, meaning Micron’s sales should stay robust into 2027.

One recent comment suggested that Micron has a great opportunity in high-bandwidth memory (HBM), which is a specific memory niche vital for AI chips. Bullish forecasts are also based on the idea that the DRAM shortage isn't finished, which should keep Micron profitable and DRAM prices up.